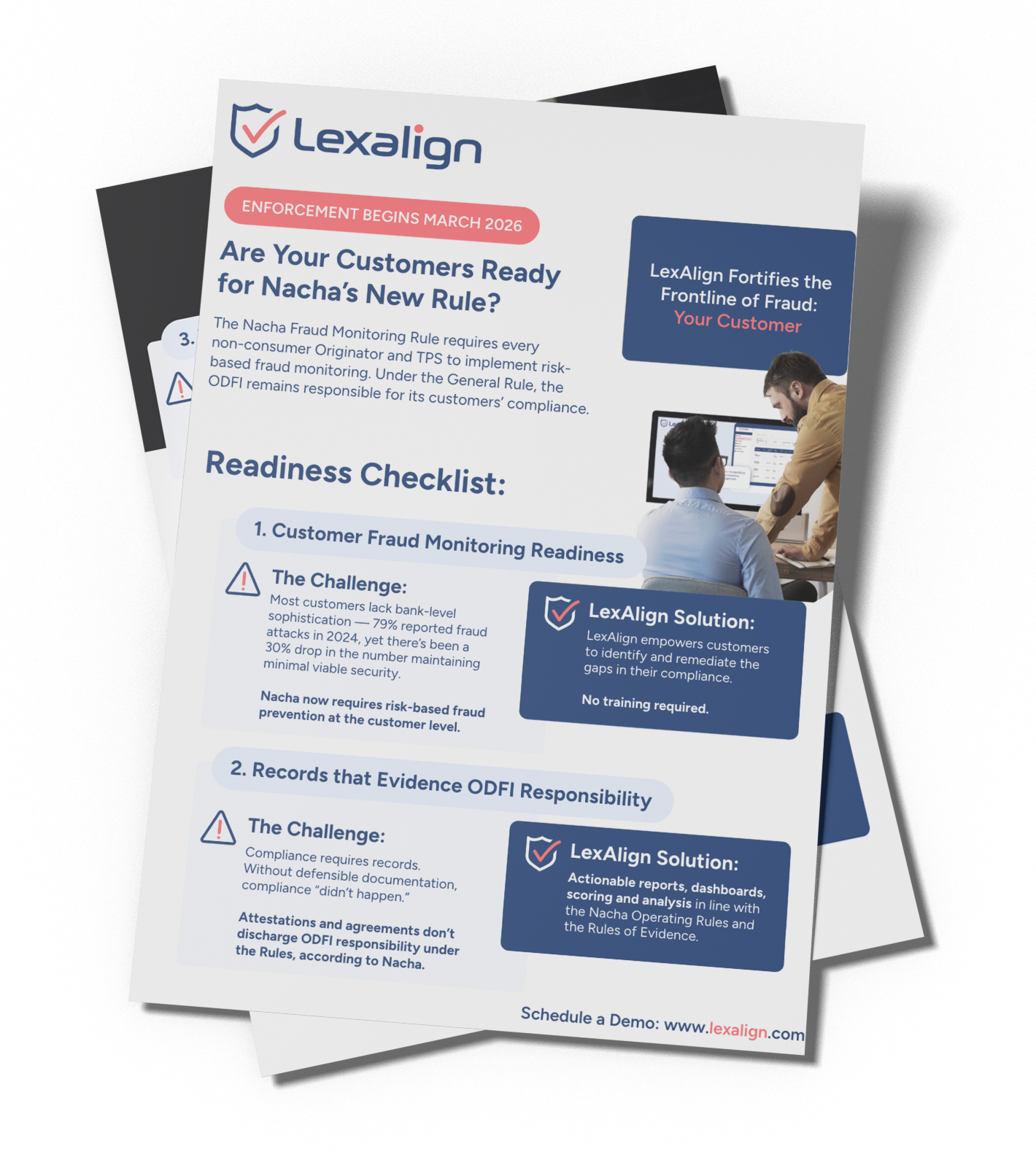

ENFORCEMENT BEGINS MARCH 2026

Lexalign is Uniquely Focused on Your Customer

The Nacha Fraud Monitoring Rule requires every non-consumer Originator and TPS to implement risk-based fraud monitoring. Under the General Rule, the ODFI remains responsible for its customers’ compliance.

LIVE OFFICE HOURS

Nacha Fraud Monitoring Rules: Office Hours for Banks

Join other financial institutions for a practical Q&A on what the new Rules mean—and how banks are operationalizing them.

FREE GUIDE

4 Boxes to Check for Nacha's 2026 Fraud Monitoring Rules

In this guide, we break the new Nacha Rules into a clear four-box framework that helps banks understand the responsibilities of each party, where existing tools need enhancing, and where gaps tend to surface—particularly around Originator controls and Third-Party Sender oversight.

ON DEMAND WEBINAR

4 Boxes to Check for Nacha's 2026 Fraud Monitoring Rules

Learn the full scope of what the Rules require and the toolkit you'll need.

LexAlign is a Preferred Partner for Compliance, Fraud Monitoring, and Risk & Fraud Prevention.

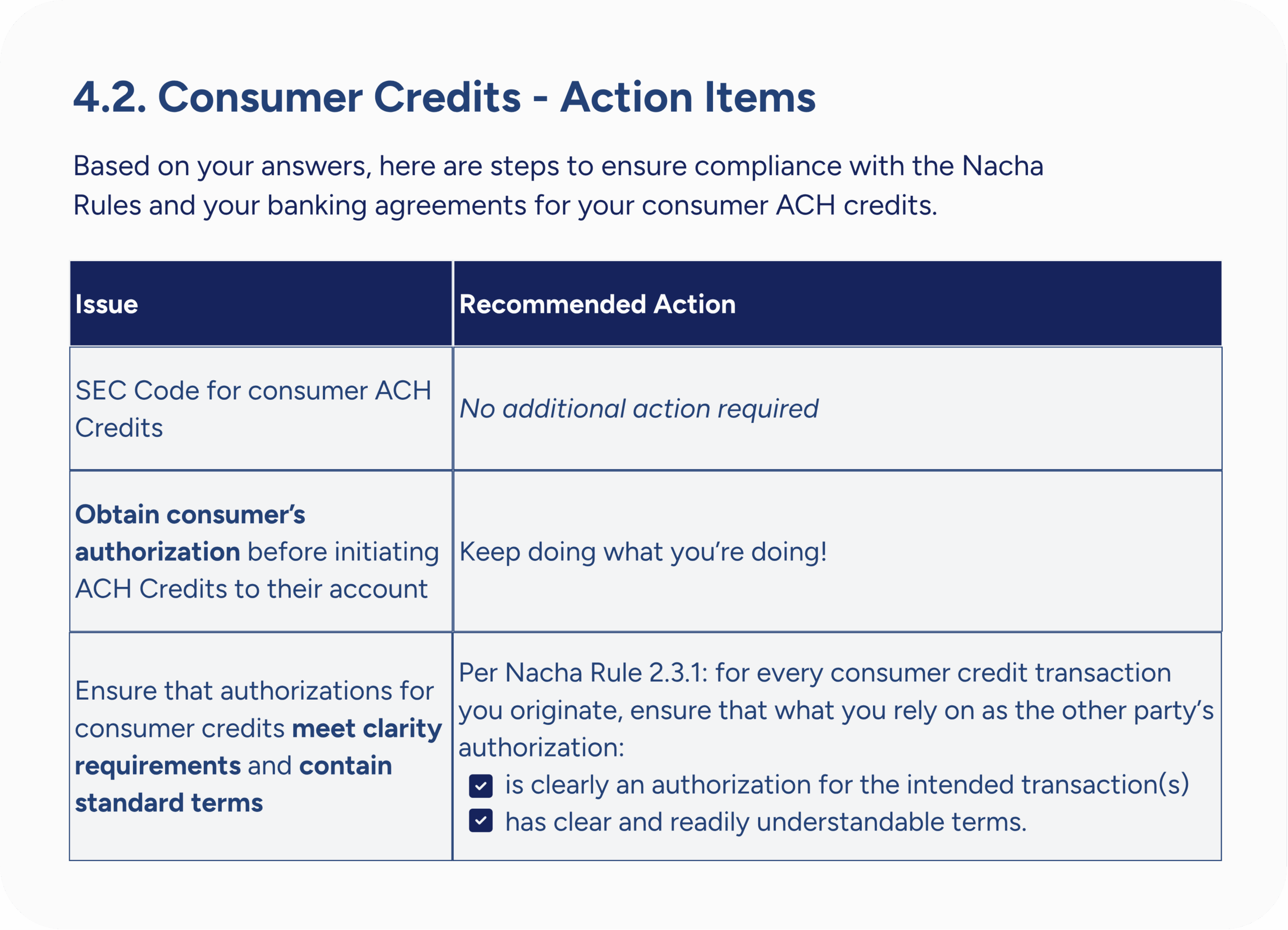

Your Customers are Responsible for Compliance

Business Originators and Third-Party Senders must maintain risk-based processes to detect unauthorized or deceptive (“False Pretenses”) payments — and review them annually.

Doing Nothing Will be Unacceptable

Nacha’s Risk Management Advisory Group (RMAG) also emphasizes that simply doing nothing is not acceptable—risk monitoring must be meaningful, documented, and operational.

Enforcement begins March 20, 2026

On March 20, 2026, the Rule is enforceable as to non-consumer Originators and Third‑Party Senders (TPS) that originated more than 6 million Entries in 2023. On June 19, 2026, enforceability extends to all remaining Originators and TPS.

GET READY FOR THE NEW RULE

How Lexalign Operationalizes Nacha’s New Fraud Monitoring Requirements

Lexalign operationalizes Nacha’s new fraud monitoring requirements into a concrete, customer-facing program that produces actionable data for both banks and their customers. Here’s how it works:

THE CHALLENGE:

Nacha Will Require Risk-Based Fraud Prevention at the Customer Level

Most customers lack bank-level sophistication — 79% reported fraud attacks in 2024, yet there’s been a 30% drop in the number maintaining minimal viable security. Nacha now requires risk-based fraud prevention at the customer level.

THE SOLUTION: Customer Fraud Monitoring Readiness

Lexalign empowers customers to identify and remediate the gaps in their compliance.

Your customers receive guided self-assessments uncover gaps

With Lexalign, your customers receive an interactive, remediation checklist to track and attest to fixes.

THE CHALLENGE:

Attestations and agreements don’t discharge ODFI responsibility under the Rules, according to Nacha.

Compliance requires records. Without defensible documentation, compliance “didn’t happen.” With Lexalign, ODFI customers receive:

THE SOLUTION: Records that Evidence ODFI Responsibility

With Lexalign, ODFI customers receive the following support in line with the Nacha Operating Rules and the Rules of Evidence:

Actionable Reports

Dashboards

Scoring

Analysis

THE CHALLENGE:

Fraud exploits gaps banks can’t see: deficient controls at the site of origination — your customer’s operations.

Lexalign Audit Reports protect banks from fraud-related liability more effectively than agreements under pertinent statutes.

THE SOLUTION: Visibility Into Customer Operations

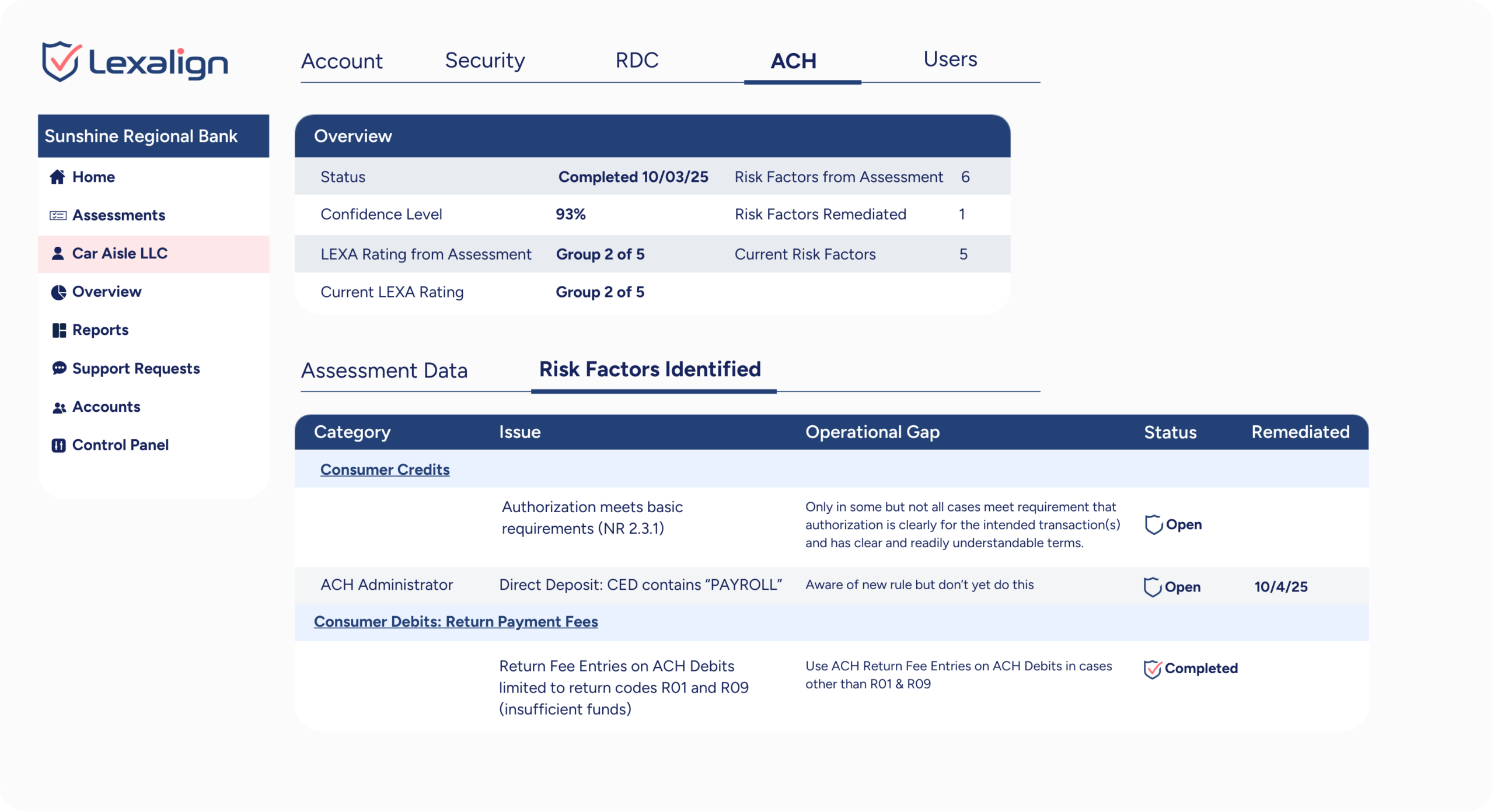

Customers complete self-assessments against the Rules and instantly obtain actionable Audit Reports

ODFIs get visibility into 80%+ of customers’ operations

On average, Lexalign users enjoy 80% assessment completion from customers

Your customers are given the tools they need to remediate their gaps.

THE CHALLENGE:

Identifying risks isn’t enough — customers need practical steps to remediate.

With Lexalign, the banks’ customers receive tailored a complete ACH Compliance Program:

THE SOLUTION: Actionable Gap Remediation

Gap Analyses & Action Plans

Policies & Procedures

Remediation Checklists

THE CHALLENGE:

ODFIs are still responsible for all originated Entries. Without proactive oversight, fines, fraud losses, and reputational risk flow upstream.

Lexalign operationalizes compliance, empowering customers to prevent fraud while enabling banks to grow faster and safer with Lexalign.

THE SOLUTION: Bank-Level Confidence, Customer-Level Action

Regulatory Alignment

Risk-Based Oversight

Low-Risk, Scalable Growth

Stronger Customer Relationships

Are You Ready for the New Rule?

Below are some resources that will help you and your team prepare your customers for Nacha’s new Fraud Monitoring Rule. Rules enforceable starting June 19, 2026.

ON DEMAND WEBINAR

The Hidden Business Case in Tooling Up for the New Nacha Fraud Monitoring Rule

Get ahead of Nacha’s new Fraud Monitoring Rule taking effect in March 2026. Learn how empowering Originator and TPS compliance can drive growth, generate non-interest income, and improve efficiency—all while meeting your own compliance obligations.

Are Your Customers Ready for the New Rule?

Download our Nacha New Rule readiness checklist to learn more about how you can be ready for the New Rule by March 2026.

Articles

LEARN MORE

Contact Us

Discover how Lexalign can streamline your workflow, reduce compliance risk, and empower your team to move faster with confidence.

Whether you’re exploring solutions or ready to upgrade your process, our product experts will guide you through a personalized walkthrough tailored to your needs.

Customers

Nacha Chose LexAlign as a

Preferred Partner for Compliance, Fraud Monitoring, and Risk & Fraud Prevention.

With LexAlign, banks don’t just “check the box” on compliance. Nacha chose LexAlign because our customers are empowered to…

Empower Customer Compliance

LexAlign identifies rules & risks specific to the customer and assesses their compliance and ability to manage the risks with actionable tasks.

Strengthen Customer Defenses Against ACH Fraud

Customers instantly get an audit report, policies, and an interactive checklist — turning vague compliance rules into clear, step-by-step actions.

Reduce Exposure to Liability When Fraud Occurs

LexAlign helps reinforce fraud defenses at the customer level and provides defensible records that satisfy examiners — reducing bank exposure under Nacha’s new rule.

Audit-Ready Compliance Records for Examiners

Get reports, policies, and remediation checklists — creating defensible, audit-ready records that examiners expect and regulators recognize as proof of compliance.